At one point or another, everyone borrows money. That’s no exaggeration, either. You borrow money to buy a car. Your parents borrowed money to buy a house. Banks borrow money. Even the federal government borrows money. Borrowing is just a fact of life, meaning that one day, your small business will probably borrow money, too. You’ll definitely want to understand the risks associated with it in intimate detail. You can learn more about those HERE. But as long as you understand and use it the right way, borrowing can be an incredible resource for your business. This article helps you wrap your head around borrowing, because knowing how and when to do it is a huge part of Marcus Lemonis’ “Know your numbers” philosophy.

How a Business Line of Credit Is Different Than a Loan

A loan has fixed terms. When you take out a loan, you borrow a set amount of money, usually from a bank. You get it right away in a lump sum, but agree to pay it back over time. Your loan agreement has three key points: the amount of money you’re borrowing, the loan term, and the interest rate. Those three factors are baked into your monthly payment and you’re locked into making that payment every single month.

Let’s say your monthly payment is $900 and your loan term is five years. Once you’ve made all 60 payments of $900, that transaction is over. But do you see how loans are dealing with fixed amounts on a fixed schedule? That’s where a loan is much different than a business line of credit.

What Is a Business Line of Credit?

A business line of credit is far more flexible. The bank gives you a limit, let’s say it’s $10,000, and you’re free to borrow however much you want as long as you stay under that limit. The reason that’s great is you’re only paying interest on what you use. Let’s say you take out a business line of credit and only borrow $1,000. That’s way under your $10,000 max. With a business line of credit, the juice is only running on the $1,000 you’ve actually borrowed. It’s fair, intuitive, and manageable. Some people call these “revolving lines of credit,” because once you hit your max, your dynamic with the lender isn’t “over.” All you have to do is pay off some of the balance, which frees up some of your credit line — and boom — you can start borrowing again.

So, when you think of a business line of credit, think of flexibility. You see this through the payments as well. Do you remember our loan example? Do you remember how you had a predetermined, fixed, monthly payment? You don’t have that with a business line of credit. Instead, your payments are informed by how much you end up borrowing, and of course, your interest rate. So, if things get slow, you don’t have some long, fixed agreement hanging over your head, like you do with a loan.

A business line of credit also gives you the flexibility to manage the amount of interest you’re paying. If you’re flush with cash one month, you can just pay off your entire balance. Then, once you have a balance of zero, you’re not paying any interest at all. This is in contrast to a loan, where you’re locked into paying interest on that entire lump sum for the entire term of the loan.

One more important thing to know is that both loans and business lines of credit are complex. You need to make sure you understand the fine print. This article is a broad overview and doesn’t account for the specifics of your situation. So, make sure you understand yours in detail. But speaking broadly, it’s safe to think of a business line of credit as far more flexible than a loan. Marcus always says, “We have to know how much money we have, what we’re spending it on, and keep track of our expenses at all times.” So, when you’re borrowing, borrow responsibly. Always, always “know your numbers” and make sure you’re borrowing in a sensible, grounded way.

How a Business Line of Credit Is Different Than a Business Credit Card

These are actually pretty similar in terms of the nuts and bolts. In both cases, you’re given a max, are free to borrow whatever you want as long as you stay under that max, and only pay interest on what you’re using. But there are a few subtle differences worth mentioning:

- With a business line of credit, you usually have to access the funds personally. But with a credit card, you can get a few copies and issue those to key employees.

- With a business line of credit, the bank wires the amount of money you’re accessing to your account. With a credit card, they don’t wire you the money. They pay the merchant for you.

- With a business line of credit, you have to track your own expenses. With a credit card, they usually offer pretty detailed reporting.

- With a business line of credit they don’t offer rewards programs. Credit cards typically do.

There are also a few differences that are a little more substantial, especially the last one:

- Business lines of credit typically have higher limits than business credit cards

- Business lines of credit are typically harder to get approved than business credit cards

- Business lines of credit typically have lower interest rates than credit cards

- Business lines of credit can typically be used for payroll, whereas credit cards usually can’t be

Secured vs. Unsecured Business Line of Credit

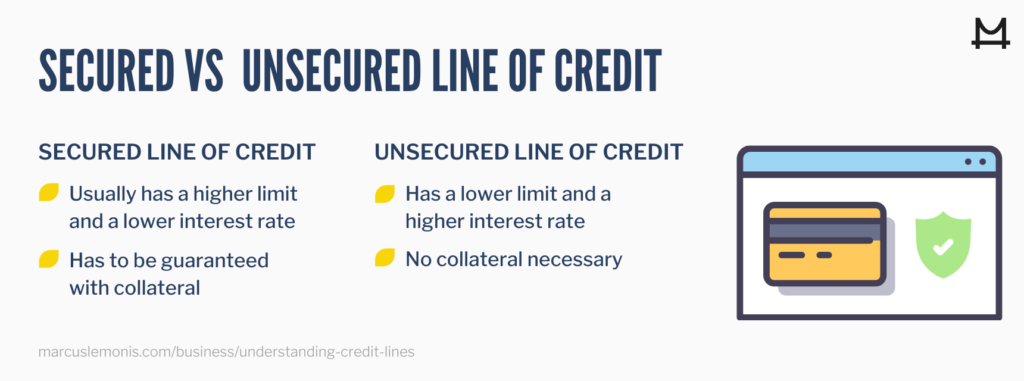

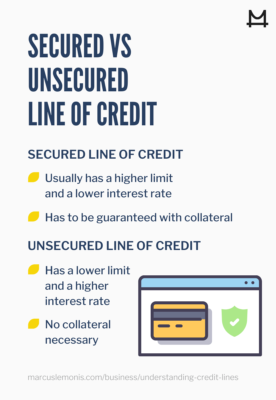

When you take out a secured business line of credit, you guarantee the money you’ve borrowed with some type of asset. That’s called “putting up collateral.” The bank just wants some sort of assurance that you’re going to pay them back. If you get in a pickle and can’t make your payments, unfortunately, the bank gets your collateral. You can use a bunch of different things as collateral, but it’s usually real estate or a vehicle. So, in plain terms, if you can’t make your payments, the bank might get your house. Or your company’s factory. Or your delivery truck .

They basically get whatever asset you formerly owned instead of your payments, which you could no longer make.

With an unsecured line of credit, you’re not putting up collateral. You still want to pay back your lender or you’ll ruin your credit. But you don’t have to give the bank your house, for example. That might make an unsecured line of credit seem like the obvious choice at first glance, but they both have pros and cons:

- A secured line of credit – the one where you guarantee it with collateral – usually has a higher limit and a lower rate. That’s because the bank is limiting their risk. They know they’ll end up with something one way or another, so they feel more comfortable lending you more money.

- On the other hand, an unsecured line of credit has a lower limit and a higher interest rate. That’s because the bank is taking on more risk. They want to be compensated for that risk, because if you can’t pay them back, that’s it. There’s no collateral coming their way.

This isn’t to scare you out of borrowing. In fact, it’s just the opposite. This article encourages you to explore business lines of credit, but to do that with a full understanding of the big picture. So, let’s take a look at a few of the ways a business line of credit can go to work for you.

The Benefits of a Business Line of Credit

You know that old saying, “It takes money to make money?” That’s the importance of a business line of credit. It gives you the money you need in order to make money. That happens in a bunch of different ways, but let’s take a look at a few different examples.

- First, let’s say you sell umbrellas and have an unexpected spike in demand. You’re in the middle of the rainiest spring on record and are selling umbrellas as fast as you can put them on the shelves. A line of credit helps you buy more inventory and take full advantage of this spike in demand.

- Next, let’s say the umbrella business is so good that you want to expand your team. When you draw on your business line of credit, that puts a corresponding amount of cash in your bank account. You’re then allowed to use that for payroll and can afford to hire another all-star.

- Third, let’s say you just sent 10,000 umbrellas to a huge school district, but they need a little more time to pay their bill. You can lean on your line of credit to make you less reliant on those unpredictable payment schedules.

- Fourth, if it doesn’t rain for all of September and umbrella sales are pretty slow, you can tap your business line of credit to help weather the storm and keep your operation running.

- Fifth, let’s say you want this fairly expensive inventory management software. It’s really pricey if you pay by the month, but if you pay for the full year up front, you get a huge discount. Your business line of credit gives you that huge chunk of money that you need to save big.

The Downside of a Business Line of Credit

As you’ve seen, a business line of credit can definitely be your friend financially. But you also want to be aware of a few things. First, you’re going to spend a decent amount on interest, as opposed to financing your business through the cash you already have on hand. So, before you tap your business line of credit, make sure you do a little math and that it justifies those interest payments. Second, if you take out a secured line of credit and can’t pay it back, you lose your collateral. Whether that’s your house, a factory, or a delivery vehicle, always remember that you’re putting this on the line. Third, if you get in over your head, you can ruin your credit. That can make it tough to open lines of credit in the future, which limits your access to all of those benefits you just read about above. So, whenever you borrow money, just remember this isn’t free. You need an actionable plan to pay this back and that plan needs to be realistic. That money sure is nice once you’re approved, but it’s like Marcus says, “You don’t get anything. You have to earn it.” So, make sure you treat this like it’s your money. Because it is.

How to Get Approved for a Business Line of Credit

Lenders look at a bunch of different things, but always dial in on a few factors in particular. First, they want to see consistent revenue. If you bring in a steady flow of cash for a few years in a row, they’re more confident you can pay them back. Second, they like to see documentation. The nature of that can vary, but they’ll usually ask for bank statements and tax returns. So, make sure you have all your ducks in a row.

Third, they’ll look into your credit score. They do this to approve your application, but also to set your interest rates. So, if your credit is in great shape, you might pay way less in interest. If this seems like a lot, don’t worry. You’ve got this. If you don’t get approved for a business line of credit, no worries. You can always apply for a business credit card, because as you’ve learned, their standards are a little more friendly for brand new businesses. All that said, take a look at a few tips that might help you get that business line of credit approved.

Tips for Getting Approved

- Put Up Collateral – If you’re having trouble getting approved, ask about secured lines of credit. Offering to guarantee your credit line with one of your assets could be just the thing that helps get that application over the net.

- Explore Online Lenders – Banks typically have more stringent requirements. They’re just larger entities with more overhead and protocol.

So, they’re typically more risk averse. But a few online lenders are aware of this and have stepped in to offer you another option. They might be more comfortable with a higher level of risk for those newer applicants.

- Boost Your Personal Credit Score – Some people are surprised to learn that when you apply for a business line of credit, the lender might also look at your personal credit score. So, make sure your house is in order on the personal side to give yourself every last advantage.

- Verify Your Application Is 100% Accurate – If you’re not sure what something means on the application, just ask. Your life is busy and you’re tracking a ton of information. But you definitely don’t want to wing it, guesstimate, or rely solely on memory. They’re making a huge decision based on the info you’re passing along, so make sure everything is perfect.

If you’re even reading this, it’s probably because your business is growing. That’s awesome. Congratulations. A little extra capital can help it grow even faster. Loans are great because you know exactly what you’re signing up for, you’ll get a fixed amount of money, and your payments are fixed as well. Business credit cards are nice because they’re easier to get approved and ideal for new businesses. But don’t forget about business lines of credit. They’re a really flexible option that you can apply towards payroll, and what’s more, you only pay interest on what you end up using. So, make sure you put time and effort into exploring all of your borrowing options, because each of them have pros and cons. It’s like Marcus always says, “You don’t have to be a genius to run a successful small business. But you better be smart enough to be willing to learn.”

This article is informational only and subject to errors or omissions. As with any legal or regulatory advice, please consult your legal counsel or tax advisor to make sure you are in compliance with all and any federal, state, city or county rules and regulations. More

- Do you have a line of credit for your business?

- Which line of credit would best fit your business’ needs?